Pandemic Fuel: The Forces Behind Maine’s Price Surge

One of the most common thoughts about the pandemic is that it accelerated changes that were already happening. Zoom existed but was not yet a dominant force. Work-from-home existed but was neither common nor expected. And the list goes on.

A variation of acceleration is accelerant—and that is what happened to home prices. The pandemic set the housing market on fire with economic stimulus plans, wildly low interest rates, forced savings, and the sudden experience of everyone working, living, going to school, and being home together. Houses that had been just fine were suddenly perceived as way too small. Interest rates that once seemed normal became unbelievably low. How could you not refinance, consider a second home, buy an Airbnb, or move somewhere you actually wanted to live?

The demand, ease, and “cheapness” of money set home prices on fire, and in Maine, the median home price went from $222k in 2019 to $376k in 2024. Normal 4% appreciation would have meant prices in 2024 would be $270k, but a few years of double-digit growth changed that dramatically.

What the Fed so incorrectly assumed was that interest rates would serve as a fire hose, capable of dampening home price inflation. We all know that didn’t work. Instead, the low interest rates created a lock-in effect: inventory dropped while demand remained strong. Interest rates went back up, but prices did not come down.

Inventory / Inflation

The price of eggs is in the news again, with bird flu resulting in the “depopulation” of flocks—and the consequent reduction in inventory. While much has been made of the price of eggs as an inflation issue, the real culprit has been housing costs. The price of homes has risen dramatically, and the cost of homeownership in the form of financing, taxes, and insurance has more than doubled.

In an article titled “The True Cost of Ownership,” the authors noted that “for consumers, the cost of money is part of the cost of living.” Therefore, when interest rates spiked to 20-year highs in the latter half of 2023, the impact was significant because home prices had risen 50% since the start of the pandemic. Since the end of 2019, the interest payment on a new 30-year mortgage is up almost threefold. As a result, household interest payments grew about 30% in 2023, the fastest rate on record.

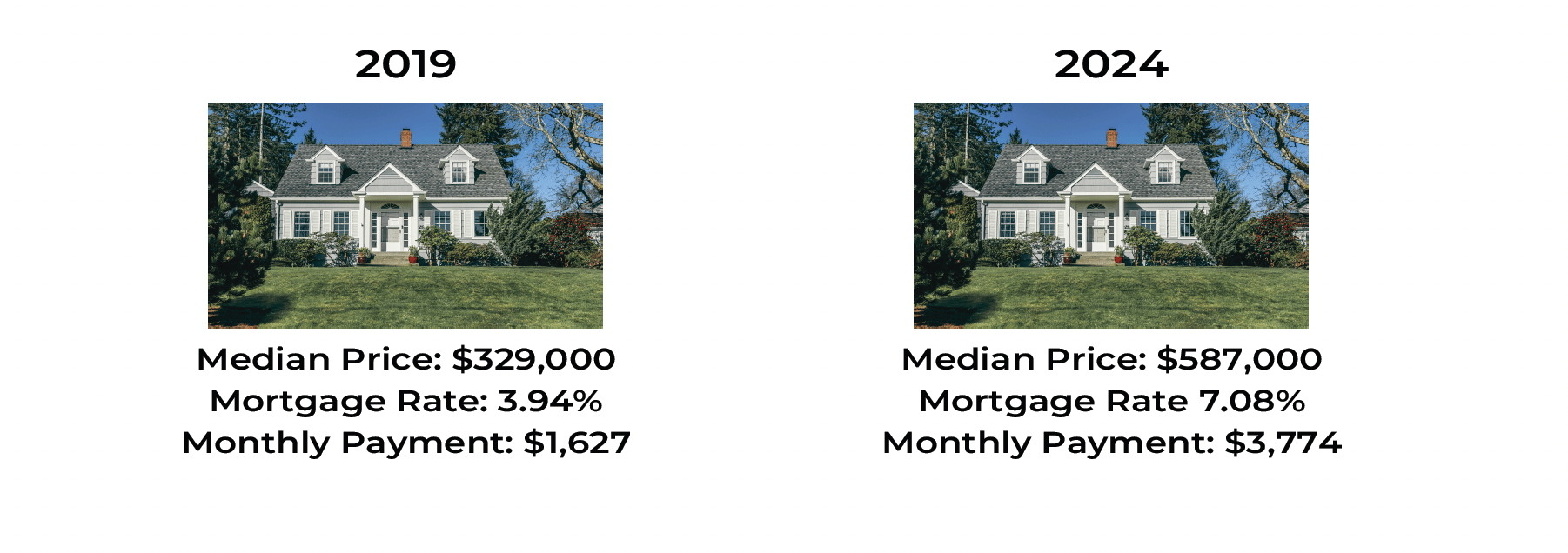

What does this look like in Portland, Maine, for a median-priced home in 2019 versus 2024?

New Construction

Inventory of existing homes is on the rise in Maine, as new listings went up in the 4th quarter by 6%, from 4,148 homes for sale to 4,402. However, newly built homes across the entire state accounted for only 315 of those sales, and only 215 of those sales were single-family homes. New construction in Maine, and across New England, is more challenging and deters large production builders who operate in the southern states and Texas, where regulations are light and costs are lower.

Consequently, we do not see large-scale developments of entry-level housing, and this has also kept prices high and increasing. In addition, Maine’s tradition of local control and the power of NIMBYs to derail projects—even those in alignment with their town code and written growth plans—has resulted in more “one-off” and higher-end new construction. Site costs are high, and it’s easier and more profitable to focus on more expensive homes. Land costs, as you will see later in this report, have jumped, and building lots in towns close to Portland can cost $200k or more. However, new homes require much less maintenance and can be more energy cost-effective as well.

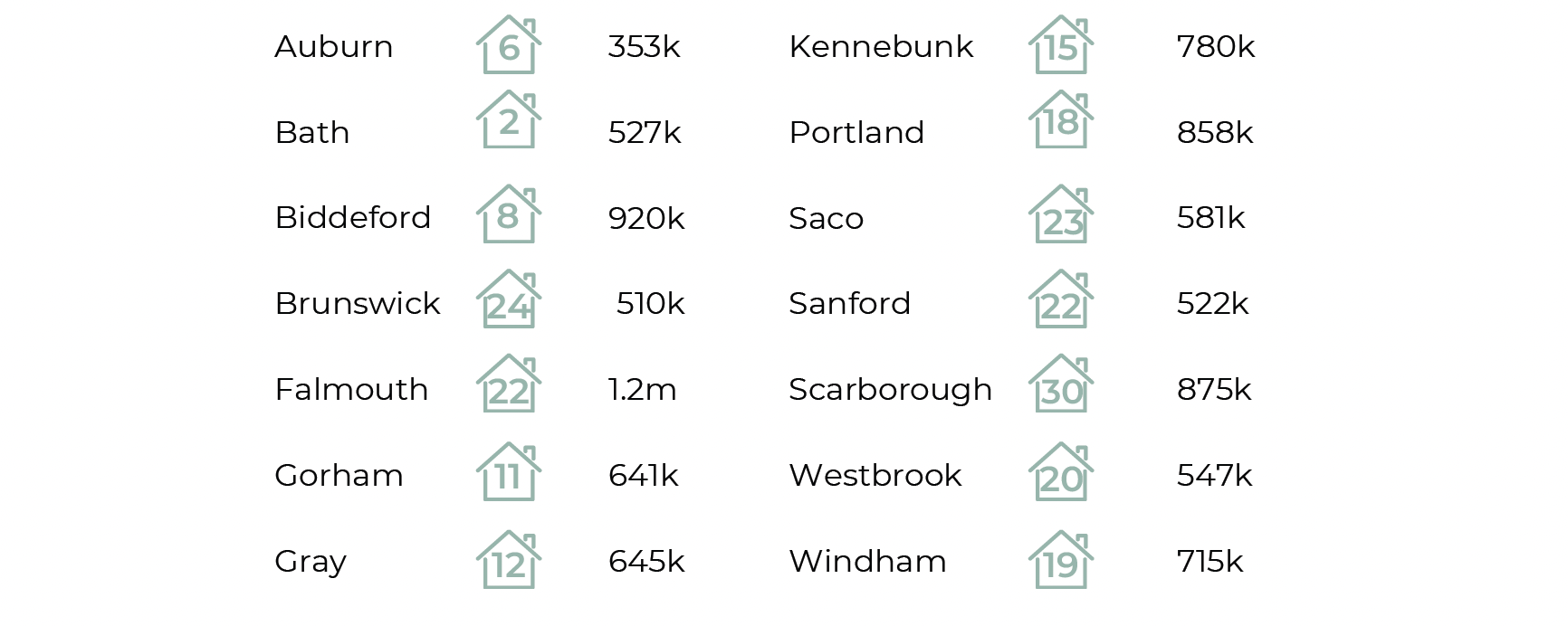

Below is a sample of new single-family homes sold in 2024 and the median price of those homes.